India’s defence sector has delivered a remarkable rally in 2025, outperforming all other sectors with a 34.8% return in the first half of the year, powered by strong government support, robust PSU performance (HAL, BEL, BDL), and a record order pipeline.

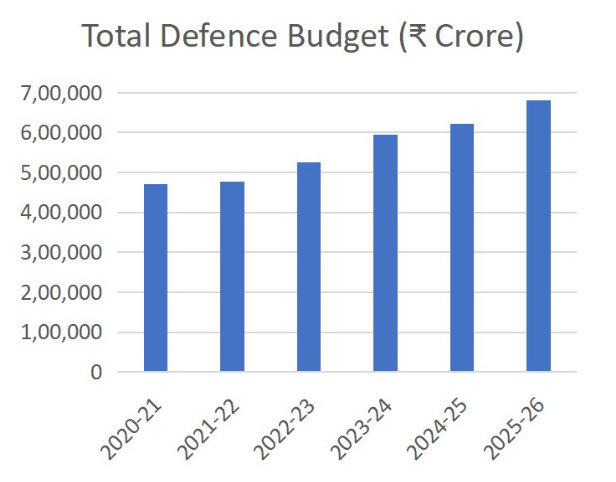

The outlook remains positive, backed by policy initiatives like Atmanirbhar Bharat, a 9.5% budget hike to ₹6.81 lakh crore, and a sharp rise in indigenisation, which have transformed India into an emerging global manufacturing hub for defence equipment.

Sector Outlook

Industry growth remains strong, with annual defence production expected to touch ₹1.75 trillion in FY25, and ambitions for ₹3 trillion by 2029.

Government initiatives—including procurement reforms, indigenisation mandates, and export promotion—are expanding global market access, notably recent exports of BrahMos missiles to Southeast Asia.

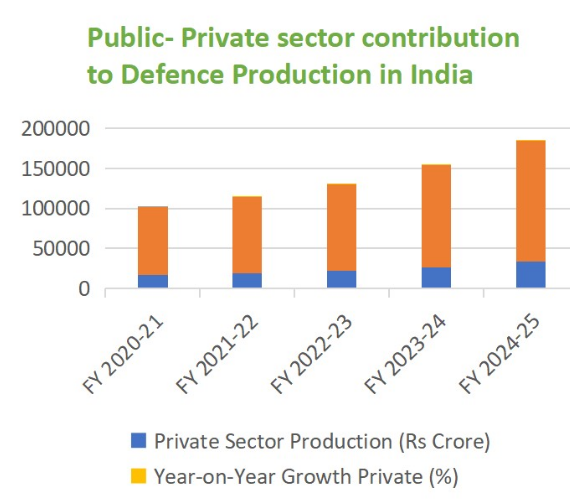

The sector is increasingly driven by rising private sector participation, which hit a record 22.56% of defence production in FY25, and R&D spending focused on next-gen technologies.

Industry overview

Key Themes

Indigenisation Drive: Positive Indigenisation Lists, Make in India policies, and Defence Industrial Corridors are pushing rapid local production and technological development, with nearly 3,000 items indigenised by early 2025.

Modernisation: Major force upgrades including induction of Tejas Mk1A fighters, new attack submarines, and advanced electronic systems; focus on Integrated Theatre Commands and operationalisation of agile Integrated Battle Groups for enhanced jointness and rapid deployment.

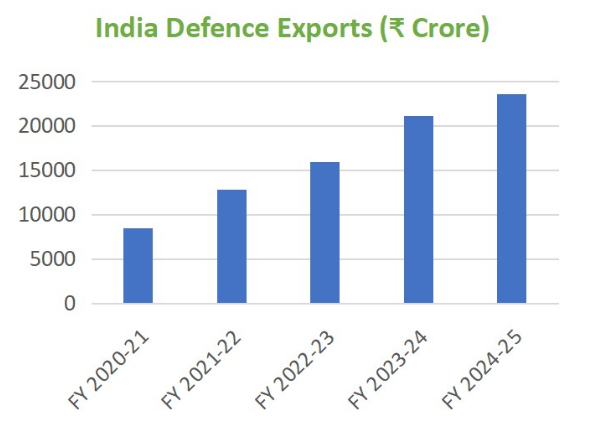

Export Momentum: Defence exports surged to ₹23,622 crore in FY25, up from ₹686 crore in FY14, with Indian platforms (BrahMos, LCH, radar systems) gaining global traction.

Major Catalysts

Policy Reform: Government procurement reforms, streamlined acquisition processes, FDI liberalisation, and innovation schemes like iDEX, promoting MSME/startup involvement.

Technology Focus: Accelerated R&D and adoption of emerging technologies such as AI, robotics, drones, electronic warfare, and cybersecurity; major procurement/development deals are supporting future-readiness.

Budget Expansion: Defence allocation reached ₹6.81 lakh crore in 2025–26, driving large-scale capability upgrades and infrastructure investments.

Geopolitical Tensions: Ongoing border challenges and regional security imperatives are prompting sustained investment in advanced platforms and deterrent capabilities.

Sector Risks

Procurement Delays: Delays in deployment due to budget constraints, bureaucratic hurdles, and slow procurement cycles.

Technology Gaps: Persistent reliance on imports for high-tech components (jet engines, missile seekers, radars) and underfunding of indigenous R&D leaves vulnerabilities.

Cybersecurity Threats: Growing digital exposure has led to major breaches—India faces a shortage of ~790,000 cybersecurity experts and lags in building robust defence architecture.

Valuation Overheating: After sharp rallies, defence stock valuations are at multi-year highs; risk of re-rating if earnings or execution falter.

Strategic Takeaways

Investors should focus on sector leaders with robust order books, high R&D intensity, and strong export potential.

Companies aligned with government reform trends and product indigenisation will maintain long-term advantage.

Continuous monitoring of procurement pipeline execution and cost controls is essential, as sector’s margin profile and stock multiples remain sensitive to project progress.

Tech-focused defence firms, those actively participating in AI, cyber, and electronics, offer highest upside given India’s push for next-gen warfare capabilities.

Export champions and companies participating in the defence corridor ecosystem are well-placed for sustained growth

Sector Growth Drivers

Global Defence Industry

Spending Trends: Global military expenditure reached a record $2.7 trillion in 2024 and will top $2.69 trillion in 2025, a 4.9% increase YoY.

Top Countries: The US, China, Russia, India, and Saudi Arabia are the biggest spenders, driven by geopolitical tensions, modernization needs, and regional conflicts.

Geopolitical Flashpoints: Regional conflicts such as Ukraine-Russia, Israel-Gaza, and China-Taiwan have pushed up capex materially.

NATO Commitments: European NATO members have accelerated defence spending towards the 2% of GDP target, with Germany, Poland, UK, and France leading upgrades and procurement.

India’s Defence Ecosystem

Role of MoD & DRDO: The Ministry of Defence (MoD) establishes policy, budget, and procurement priorities. DRDO drives indigenous R&D, with 60+ labs and major projects like Tejas, Akash, and missile systems.

DPSUs & Private Players: DPSUs (HAL, BEL, BDL, MDL, GRSE) dominate, contributing over 70% of domestic output. Private sector share hit a record 23% in FY25, with Tata Advanced Systems, L&T, Adani, and Bharat Forge ramping up capacities and exports.

Foreign OEM Tie-Ups: Strategic partnerships with global OEMs—Lockheed Martin, Boeing, Airbus, Rafael, MBDA—enable co-development, joint ventures, and technology transfers.

Defence Budget Analysis

FY 2025–26 Allocation: Defence budget is ₹6,81,210 crore ($77.4 bn), up 9.5% YoY.

Modernisation Outlays: ₹1,11,545 crore (75% of modernization spend) earmarked for domestic procurement—reflecting a sharp push for self-reliance and import substitution.

Procurement Trends: India continues multi-year programs for fighters (Tejas Mk1A), ships (scorpene submarines), drones, electronics, missiles, and integrated battle systems.

Policy Landscape

Reform Initiatives:

DAP 2020: Streamlines procurement, enhances digital monitoring, promotes local sourcing, and flexibility in offset partners.

Make in India: Encourages local manufacturing, with Positive Indigenisation Lists and higher procurement from Indian firms.

iDEX: Incentivizes startups/MSMEs for innovation grants and rapid prototype development in UAVs, AI, sensors, and simulation.

Defence Corridors: Six industrial corridors (Uttar Pradesh, Tamil Nadu) catalyse cluster-based manufacturing and export-oriented growth.

FDI Policy: Automatic FDI up to 74%, allowing greater foreign capital and tech inflows.

Offset Norms: DAP 2020 introduces flexible offset multipliers to attract investment/technology transfer, favoring MSMEs and critical tech adoption.

Demand-Supply Dynamics

Armed Forces Modernization Programs

India has launched a 15-year modernization plan (2025–2040) focused on comprehensive upgrades across Army, Navy, and Air Force.

Army: Inducting 1,800+ main battle tanks, light tanks, artillery rounds, and multiple unmanned aerial systems (UAVs) for enhanced ground combat and ISR capabilities. Emphasis on digitization and integrated battle networks.

Navy: Building blue-water capability with nuclear-powered carriers, 10+ next-gen destroyers, amphibious landing platforms, and advanced helicopters.

Air Force: Acquiring 400+ combat aircraft (Tejas Mk1A, Rafale,AMCA), 350 multi-mission drones, stealth unmanned combat aerial vehicles (UCAVs), high-power lasers, and directed energy weapons. Cyber defense and space-based offense capabilities are being integrated.

Procurement Pipeline

The Ministry of Defence conducts transparent procurement through eProcurement portals with ongoing RFPs, RFIs, and tenders for platforms and subsystems, including artillery guns, missiles, naval vessels, and avionics.

FY25 pipeline showcased 193 contracts worth ₹2.09 lakh crore, with domestic firms securing 92% of contracts reflecting the Atmanirbhar push.

Future tenders include air defense systems, UAVs, electronic warfare suites, and ground combat vehicles aligned with the 15-year modernization.

Domestic vs Foreign Supplier Share

India historically imported about 65-70% of defence equipment but domestic sourcing rose to roughly 65% by 2025 due to indigenization and policy reforms.

Domestic Production: 16 DPSUs, 21% private sector share, ~400+ licensed private companies, and 16,000 MSMEs have emerged as strong contributors to local production.

Private sector’s role is growing rapidly due to government incentives and export orientation, reducing reliance on foreign OEMs and imports.

Foreign OEMs still play critical roles through partnerships, technology transfers, and joint ventures, notably in platforms requiring advanced tech (fighter jets, submarines, missiles).

Capacity, Manufacturing Ecosystem, and Supply-chain

Defence Industrial Corridors in Uttar Pradesh and Tamil Nadu provide integrated facilities, improving scale, supply chain efficiencies, and skilled workforce availability.

Key regional hubs specialize in aerospace (Bengaluru), missile & EW systems (Hyderabad), armoured vehicles (Pune), naval shipbuilding (Chennai, Goa, Kochi, Mumbai), strengthening India’s defence manufacturing ecosystem.

Supply chain bottlenecks remain in critical microelectronics, specialized alloys, and precision components, but government-backed R&D and industry consortia are addressing gaps.

Increasing emphasis on cybersecurity, software integration, and AI-enabled manufacturing is transforming traditional production processes in defence.

Competitive Landscape

Major DPSUs

Hindustan Aeronautics Limited (HAL): Leads in aerospace manufacturing, producing Tejas fighter jets, helicopters, and aero-engines. FY25 revenue stood around ₹30,105 crore with 7% YoY growth; it boasts a massive order book and strong R&D focus.

Bharat Electronics Limited (BEL): Specializes in defence electronics, radars, communication systems, and missile subsystems. It posted ₹7,165 crore order book as of FY25, targeting 15–17.5% revenue CAGR and >20% profit growth.

Bharat Dynamics Limited (BDL): Manufactures missile systems and ammunition, key supplier for Indian armed forces and exports.

Garden Reach Shipbuilders & Engineers (GRSE) and Mazagon Dock Shipbuilders (MDL): Premier naval shipyards driving India’s naval modernization with contract wins for frigates, submarines, and destroyers.

Large Private Players

Larsen & Toubro (L&T): Has a growing defence division focused on missiles, naval platforms, and electronics, leveraging its EPC and systems integration expertise.

Bharat Forge: Manufactures automotive and defence components, expanding into aerospace and artillery munitions with technology collaborations.

Tata Advanced Systems Limited (TASL): Is a leading aerospace and defence systems player with capabilities in UAVs, missile systems, radars, and avionics; it partners globally with Lockheed Martin, Boeing, and others.

New-age Players

Paras Defence & Space Technologies: Specializes in optics, drones, electronic warfare, and space-grade electronics with a CAGR revenue growth of nearly 20% over 5 years and improving profitability.

Data Patterns: Focuses on electronic warfare, C4ISR systems, and space electronics, rapidly scaling with ₹730 crore order book and plans for ₹150 crore capex.

ideaForge: Is India’s largest drone manufacturer with market-leading UAVs deployed by defence and para-military forces.

Tonbo Imaging: Develops ruggedized electro-optical sensors and imaging systems with increasing defence and export traction.

Peer Benchmarking Overview

Financial Strength & R&D: Large DPSUs balance moderate margins with vast scale and deep R&D spend; private and new-age companies show higher margin and ROCE volatility but stronger innovation and growth potential.

Order Book Visibility: DPSUs command massive, multi-year government orders supporting stability; private/new-age firms leverage export growth and niche tech plays driving rapid order book accretion.

Sector Niche: DPSUs dominate scale and legacy platforms. Private firms excel in tech-intensive segments (UAVs, EW, missiles) and exports, reflecting India’s shifting defence industrial landscape.

Financial & Valuation Analysis

Sector-Level Financial Metrics

Revenue Growth: Indian defence companies are poised for 16-18% revenue CAGR in FY26, continuing strong momentum from 20% CAGR during FY22–25. Growth is driven by rising government budgets, indigenization policies, and export demand. Private firms particularly show accelerated growth backed by robust order inflows.

Margins: Operating profit margins broadly range from 18% to 31% depending on product mix and company scale. DPSUs like HAL and BEL have margin stability near 25-30%, while new-age tech firms boast higher EBITDA margins (~35-40%) on niche products.

ROE/ROCE: ROCE across DPSUs averages 15-25% with HAL at the higher end (~22-25%), while private players achieve ROCE upwards of 18-25% due to asset-light models and leaner operations.

Working Capital Trends: Defence companies typically have working capital cycles of 75-120 days driven by governmental payment terms and inventory requirements. Recent reforms have improved payment discipline, but incremental working capital debt is reported given rising scale and contract staging.

Key Company Financial Model Summaries

Hindustan Aeronautics Ltd (HAL): FY25 revenue ₹30,105 Cr, EBITDA margin 27%, PAT ₹3,869 Cr, order book ~₹1.8 lakh Cr; strong capex and R&D spend (~3-4% of revenue) to scale aerospace capacity.

Bharat Electronics Ltd (BEL): FY25 revenue ₹23,024 Cr, EBITDA margin ~29%, PAT ₹5,288 Cr, order book ~₹71,650 Cr; high export and new product revenue mix driving growth.

Bharat Dynamics Ltd (BDL): FY25 revenue ₹3,345 Cr; niche missile manufacturing drives steady margins ~23-25%, strong dividend payout ratio, order book ₹22,814 Cr supporting 2-3 year visibility.

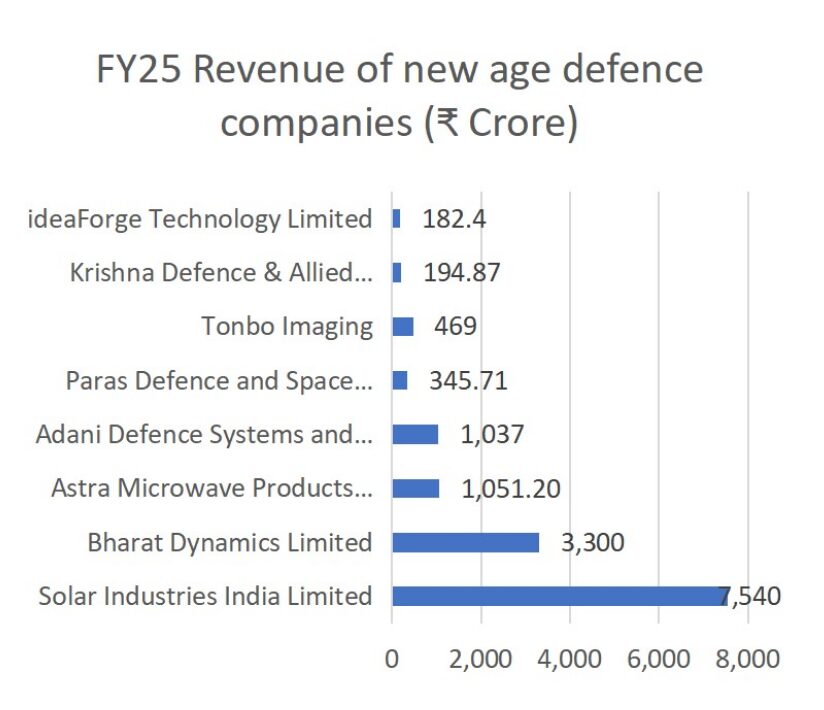

Paras Defence: Smaller scale with ₹365 Cr revenue; EBITDA margin near 39%, driven by optoelectronics and drone product lines; rapid order book growth and export diversification underway.

Data Patterns: FY25 revenue ₹755 Cr, 36% EBITDA margin, ROCE around 16%, supported by tech modernization contracts and export wins.

Valuation Methods

Discounted Cash Flow (DCF): Favored for long-term intrinsic value estimation. Assumptions include revenue growth trajectory, margin normalization, capex estimate, and weighted average cost of capital (WACC). Suitable for DPSUs with stable cash flows or private firms with visible order pipelines.

EV/EBITDA & P/E Ratios: Common market multiples used for relative valuation. Defence stocks tend to trade at premium EV/EBITDA (15-25x) and P/E ratios (~35-50x) reflecting their growth prospects, strategic importance, and order book visibility.

Price-to-Book (P/B): Useful for asset-heavy firms like shipyards. Typically ranges from 2x to 6x depending on tangible asset base and earnings quality.

Sensitivity Analysis & Target Multiples

Sensitivity analysis models factoring variations in revenue growth (±2-3%), margin expansion/contraction (±100-200 bps), capex intensity, and working capital changes help assess intrinsic value volatility.

Target multiples for strong DPSUs reflect 20-25% expected earnings growth, with P/E multiples of 35-45x justified for companies with superior order books, technological differentiation, and export momentum.

Private and niche technology firms carry higher valuation multiples (EV/EBITDA 25-40x) given faster growth but elevated execution risks.

Monitor risks including procurement delays, policy shifts, and geopolitical tensions that directly impact defence sector cash flows and valuations.

Sub-Sector Breakdowns

Aerospace & Aviation (HAL, BEL Avionics)

Hindustan Aeronautics Limited (HAL) is India’s flagship aerospace manufacturer, producing Tejas light combat aircraft, Dhruv helicopters, and aero-engines. FY25 marked major contracts including 97 Tejas Mk-1A jets (₹62,000 cr) and ongoing engine development programs, with an order book nearing ₹1.9 lakh crore.

Bharat Electronics Limited (BEL) supplies avionics, radars, electronic warfare systems, and communication suites integral to aircraft systems. BEL recorded a ₹71,650 crore order book, with exports contributing ~5% to revenues, strengthening coastal and aerial surveillance capabilities.

The aerospace sector is driven by modernization, import substitution, and technology transfers embedded into platform manufacturing, making it a strategic growth pillar.

Shipbuilding & Maritime Defence (MDL, GRSE, L&T)

Mazagon Dock Shipbuilders (MDL) and Garden Reach Shipbuilders & Engineers (GRSE) dominate naval shipbuilding, constructing frigates, destroyers, submarines including Scorpene-class vessels. Both maintain order books over ₹22,000 crore.

L&T’s shipbuilding arm complements these with platforms for Indian Navy and Coast Guard. Recent government maritime push of ₹70,000 crore for shipbuilding infrastructure supports capacity expansion.

The sector outlook is strong with export potential for smaller vessels and infrastructure status lowering financing costs for capital-intensive projects.

Missiles & Ammunition (BDL, Solar Industries)

Bharat Dynamics Limited (BDL) is the premier missile manufacturer, producing Akash, Astra, VL-SRSAM, and other missile systems, supported by an order book near ₹22,814 crore, driving strong revenue and margin growth.

Solar Industries India specializes in explosives, detonators, and ammunition components, scaling rapidly on increasing defence and civilian demand, contributing to the secure production ecosystem of munitions.

Electronics & Sensors (BEL, Data Patterns, Astra Microwave)

BEL leads defence electronics manufacturing with a diversified portfolio in radars, naval sensors, communication and EW systems.

Data Patterns focuses on advanced electronic warfare, avionics, and C4ISR systems, backed by technological innovation and defense contracts.

Astra Microwave Products produces microwave and radar systems, essential for missile guidance and surveillance platforms. All benefit from government programs targeting layered area defence and network-centric warfare capabilities.

Simulation, Drones, UAVs, and Surveillance (Zen Technologies, ideaForge, Paras Defence)

Zen Technologies specializes in defence simulators for army, navy, and air force training with a rapidly expanding export footprint.

ideaForge is India’s largest drone manufacturer, providing tactical UAVs for surveillance and combat support.

Paras Defence is focused on electronic warfare, drone technology, and optoelectronics, reporting robust revenue growth and order accumulation.

This sub-sector benefits from increased focus on AI, unmanned systems, and real-time battlefield awareness, critical for future warfare.

India allows FDI up to 74% under the automatic route for defence manufacturing companies seeking new industrial licenses, an increase from the prior 49% cap. FDI beyond 74% requires government approval, especially when it involves access to modern technology.

Industrial license applications are processed by the Department for Promotion of Industry and Internal Trade (DPIIT) with input from the Ministry of Defence and Ministry of External Affairs. Security clearances by Ministry of Home Affairs are mandatory for foreign investments.

The Make-in-India in Defence initiative aggressively promotes domestic manufacture, with a growing Positive Indigenisation List restricting imports of key items. Procurement policy mandates increasing Indigenous Content levels (50-60%) for defence contracts under DAP 2020.

The SRIJAN portal facilitates transparent tracking of indigenization progress and vendor registration, fostering MSMEs and startups in the defence supply chain.

DAP 2020 aims to simplify procurement through institutional mechanisms, digital tendering, and enhanced indigenous content mandates. It classifies procurements into five categories encouraging Make, Buy Indian-IDDM (Indigenously Designed Developed and Manufactured), Buy Indian, Buy Global.

Procurement contracts stipulate a minimum Indigenous Content (IC) of 50-60% depending on category, driving local manufacturing and technology development.

Defence exports are governed by the Defence Export Promotion Policy (DPEPP) 2020, which targets USD 5 billion of exports by 2025. Authorizations are provided via DDP (Defence Development and Production Policy) and streamlined through the Open General Export License (OGEL) for eligible items.

The government provides export facilitation through standard operation procedures, quality certifications, and R&D support.

Public-Private Partnerships (PPPs) are a core pillar under Atmanirbhar Bharat, encouraging collaboration between DPSUs, private industry, and academia in defence R&D, manufacturing, and innovation. The Technology Development Fund (TDF) and other schemes provide grants and capital subsidies for MSMEs and startups.

The Defence Testing Infrastructure Scheme (DTIS) launched in 2020 with ₹400 crore outlay, aims to establish world-class test centres and qualification infrastructure to support indigenous development, lowering dependence on foreign testing facilities.

State-of-the-art ranges for missiles, aeronautics, electronic warfare, and naval systems are being built/upgraded nationwide with government funding and private collaboration.

R&D Collaboration Policies

DRDO fosters industry-academia collaborations via Advanced Technology Centres (ATCs) and Centres of Excellence (CoEs), promoting Directed Research in advanced warfighting tech including AI, cyber, hypersonics, and space defence.

Procurement policy encourages inclusion of R&D components in contracts and incentivizes Make-II and Make-I projects to nurture private sector innovations and indigenous product development.

AI, Autonomous Drones, Directed Energy Weapons, EW Systems

AI Integration: India’s military is shifting rapidly toward artificial intelligence for battlefield awareness, logistics, predictive maintenance, and C4ISR (Command, Control, Communication, Computer, Intelligence, Surveillance, and Reconnaissance) operations. The Defence AI Council and Centre for Artificial Intelligence & Robotics (DRDO) drive adoption, using AI for sensor fusion, drone swarms, and operational command.

Autonomous Drones: India fields indigenous drones like HAL’s CATS (Combat Air Teaming System) and NewSpace MBC2 AI-powered swarming drones, plus imported MQ-9B and Heron platforms for long-range ISR. Unmanned systems enable deep-strike and border surveillance, and AI-powered coordination is now central to multi-domain operations.

Directed Energy Weapons (DEWs): India joined the elite group that fields battlefield-ready laser weapons after DRDO’s successful MK-II(A) DEW test in April 2025. Projects like DURGA II, Surya (300kW), and KALI are designed for counter-drone, anti-missile, and Star Wars-type scenarios—offering rapid, high-impact defense against hypersonic aerial threats.

Electronic Warfare (EW) Systems: BEL, Data Patterns, Paras Defence, and Astra Microwave lead India’s push for EW dominance—radars, jammers, and C4ISR platforms are increasingly AI-driven and built for countering both conventional and cyber threats.

3D Printing, Space-Based Defence Systems, Cybersecurity

3D Printing: Indian DPSUs and private firms now use advanced additive manufacturing for spare parts, missile components, and rapid prototyping. This reduces costs, enhances supply chain resilience, and accelerates R&D cycles.

Space-Based Defence: India’s upcoming deployment of small satellites and military constellations strengthens both strategic comms and surveillance. Space-driven missile early warning, navigation, and targeting capabilities are being field-tested by DRDO and allied agencies.

Cybersecurity: Rapid digitalization in C4ISR, border monitoring, and unmanned systems has made cybersecurity a top priority. AI-powered cyberdefense platforms, secure data networks, and hardened comms protocols aim to prevent breaches and maintain battlefield integrity.

Dual-Use Technologies and Civilian Spin-Offs

Dual-Use Innovations: Advanced navigation, secure communications, drone technology, and cyber solutions developed for the military are being commercialized for civilian markets—enabling growth in logistics, energy management, and disaster relief.

DRDO’s efforts in technology transfer and collaborative R&D are enabling start-ups and established industries to apply military-grade solutions in industry, healthcare, agriculture, and public safety, accelerating innovation and export potential.

Investors increasingly favor dual-use startups due to diversified market opportunities, faster revenue cycles, and broader technological impact beyond defence contracts.

Key risks

Policy Delays: Procurement procedures such as Defence Acquisition Procedure (DAP 2020) and approval processes can face bureaucratic delays, slowing modernization.

Geopolitical Shocks: Conflicts or diplomatic strains can abruptly change procurement priorities and export markets, introducing volatility.

Dependence on MoD Funding: Heavy reliance on government defense budgets makes the sector vulnerable to fiscal shifts or budget cuts due to economic pressures.

Regulatory Bottlenecks: Complex licensing, FDI approvals, and security clearances can stymie private sector growth and foreign collaborations.

Technology Obsolescence: Rapid evolution in warfare demands continuous R&D investments; failure to keep pace risks product relevance and market share loss.

Outlook & Conclusion

3–5 Year Sector Outlook

Indian defence sector revenues are expected to grow at a 16-20% CAGR over the next 3–5 years, propelled by sustained government budget increases, indigenization acceleration, and export market expansion.

Order inflows will remain robust owing to long-term modernization plans across Army, Navy, and Air Force, with a projected order book growth to over ₹4 lakh crore by FY30 from ₹2.5 lakh crore in FY25.

Margin profiles are likely to improve modestly with increased domestic manufacturing scale and higher value-addition, while higher R&D spending will enable competitive product evolution.

DPSUs like HAL, BEL, and BDL will continue commanding large government contracts, but private sector & new-age firms will see faster revenue growth and market share gains, especially in tech-intensive subsectors such as drones, electronic warfare, and AI-enabled systems.

Final Investment Stance: Overweight

The Indian defence sector presents an attractive risk-return profile with secular growth drivers from government policy thrust, geopolitical imperatives, and indigenous innovation.

Despite elevated valuations for many large-cap stocks, the sector is recommended as Overweight for long-term investors targeting 15-20% CAGR returns backed by improving earnings visibility and order pipeline.

Portfolio allocation should emphasize a mix of marquee DPSUs for stability and private/new-age tech firms for growth, with active monitoring of execution risks and regulatory developments.

Investors should watch for valuation resets triggered by policy clarity, export wins, and technological breakthroughs as rerating catalysts.

Sector-Level SWOT Summary

Strengths

Weaknesses

– Robust government commitment with 9.5%+ budget growth and ₹6.81 lakh crore allocation in FY26

– High dependence on Ministry of Defence (MoD) funding and procurement timelines

– Strong push for Atmanirbhar Bharat and indigenization driving reduced imports and technology transfer

– Lengthy procurement cycles and policy delays constrain project execution

– Presence of large DPSUs with strong balance sheets and order books offering stability

– Limited private sector scale compared to global peers; technology gaps in critical areas

– Rapid growth in exports (₹23,622 crore in FY25) boosting global competitiveness

– Supply chain bottlenecks persist in high-tech components and materials

– Emerging new-age technology firms in AI, drones, EW, and cyber systems creating innovation

– Vulnerability to technological obsolescence amid fast-changing warfare tech

Opportunities

Threats

– Increasing global defence market size and India’s growing share via exports and co-development

– Geopolitical shocks causing unpredictable shifts in procurement and budgeting

– Growing private sector involvement and MSME/startup ecosystem fostering innovation

– Potential weakening of defence budget or slow policy reforms impacting growth

– Advancements in AI, autonomous systems, directed energy weapons, and space defence

– Regulatory bottlenecks and licensing complexities delaying commercialization

– Government initiatives like Defence Corridors, iDEX, and Technology Development Funds

– Dependence on foreign OEMs for core technologies and risk of technology denial

– Civilian spin-offs of dual-use technologies expanding market and earnings diversity

– Cybersecurity threats impacting defence infrastructure and data integrity

The stocks mentioned here are for informational purposes only and should not be considered recommendations. Please do your research and analyze stocks thoroughly before making any investment decisions. Jainam Broking Limited does not guarantee assured returns or future performance of any securities or instruments.

Open Free Demat Account!

Join our 3 Cr+ happy customers

₹0

Brokerage For first 30 days*

About the Author

Know the mind behind this article

Jainam Resources

Jainam Resources is a knowledge initiative by Jainam Broking Limited aimed at empowering i...